Despite its leading role in advancing financial inclusion on a continent where banking penetration remains low, mobile money still faces major structural barriers that limit its full potential. Yet the service, which continues to expand with new offerings, particularly in banking, has the capacity to transform household economies and the broader financial landscape in Africa.

Africa's mobile money sector recorded strong growth in 2025, yet barriers to full adoption persist for millions across the continent.

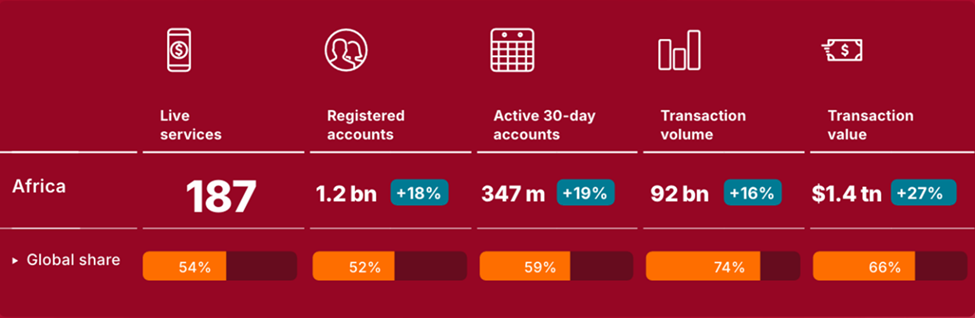

Nearly $1.432 trillion flowed through mobile money accounts in Africa in 2025, up roughly 27% from 2024, according to the "State of the Industry Report on Mobile Money 2026," published Tuesday, March 24, by the GSMA, the global association of mobile network operators.

The continent accounted for nearly 66% of the $2.091 trillion in global mobile money transaction value, which itself rose 23% year on year. Africa also represented around 74% of the 125 billion mobile money transactions recorded worldwide, roughly 92 billion operations, up 16% from 2024.

The report also noted that Africa is home to 52% of mobile money accounts globally. At end-2025, the continent had approximately 1.2 billion accounts, up 18% from 2024, with 347 million active on a monthly basis. Worldwide, total accounts reached around 2.3 billion, up 13%, with 593 million active over a 30-day period.

Africa remains the epicenter of mobile finance. But this success masks a growing contradiction: the service is expanding rapidly while full adoption across the population and its real impact remain limited.

Barriers to inclusion

The first barrier is access to devices. The World Bank notes that 84% of adults in developing countries own a phone, but roughly one quarter of them still use a basic handset, "more affordable, with limited features and no internet browser." Only two-thirds of adults therefore own a full smartphone enabling access to apps and browsers. In sub-Saharan Africa, that figure drops to 33%. In that region, as in South Asia, the most commonly cited reason for not owning a smartphone is cost. The International Telecommunication Union (ITU) has also highlighted that across the African continent, one of the main obstacles to the adoption of digital services remains affordability, particularly that of devices.

The second barrier is digital financial literacy. The GSMA's 2026 mobile money report is explicit: low digital financial literacy remains a major obstacle to the adoption and use of the service. In African countries surveyed where uptake gaps persist, the data are clear. In Ethiopia, among people who are aware of mobile money but do not have an account, 60% of women and 54% of men say they do not know how to use the service; 45% of women and 50% of men say they struggle to use a phone or fear making mistakes. In Egypt, this barrier affects 21% of women and 15% of men; in Nigeria, 22% of both women and men. Compounding this, in Ethiopia, 24% of women surveyed cite the lack of a SIM card or phone as an obstacle.

Beyond the service, a human impact

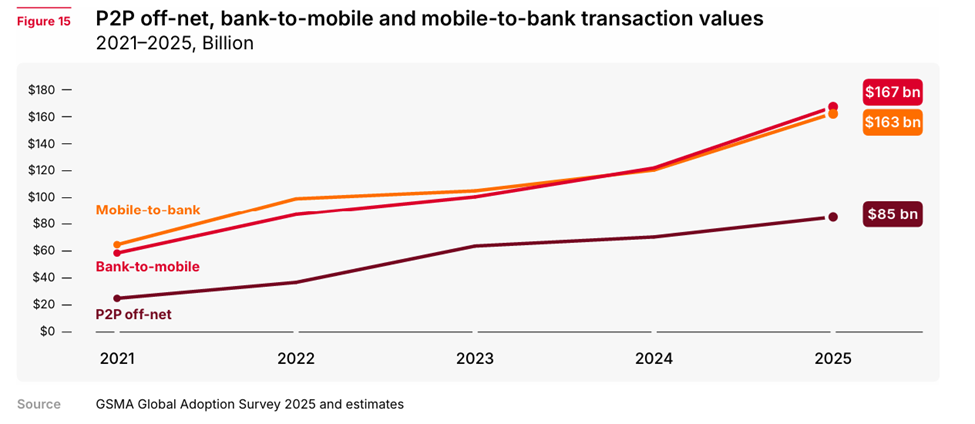

A clear paradox emerges: mobile money first took hold through the most basic handsets. But its new frontier now demands more than a simple mobile phone. The range of use cases has expanded, and service providers increasingly rely on super-apps rather than USSD codes to deliver greater value, including bill payments, government social transfers, micro-insurance, micro-credit and micro-savings. The most dynamic segments are now merchant payments, up 42% to $155 billion in 2025, and interoperable transfers between banks and mobile wallets, at $167 billion. In other words, the sector has moved well beyond the simple peer-to-peer transfers of its early days, advancing into a more sophisticated phase where users must navigate interfaces, options, QR codes, virtual cards, security features and transaction records. Without adequate devices or basic digital fluency, a portion of Africans risk being confined to the most elementary uses as the ecosystem moves toward more complex services.

This divide is also social and gendered. Without suitable phones and basic digital skills, millions of Africans remain on the margins of what mobile money can offer. In low- and middle-income countries, the GSMA estimates that women remain 14% less likely than men to use mobile internet, leaving 885 million women still unconnected, of whom approximately 60% live in South Asia and sub-Saharan Africa. This creates the risk of a two-speed financial inclusion, uneven in practice.

Unlocking the full potential of mobile money in Africa therefore requires more than a commercial response. It must be industrial, educational and regulatory. The ITU advocates for cheaper entry-level smartphones, purchase options facilitated through microcredit or installment payments, lower costs for handsets and data, and the integration of basic digital skills into school curricula and training programs. The GSMA report echoes this view, stressing the need for digital financial literacy initiatives targeting women, rural populations and older people. The World Bank notes that cost, ease of use and security must be addressed together. The real challenge for Africa is no longer to prove that mobile money works, it is to ensure that everyone can genuinely use it.

Muriel Edjo