Finance (117)

-

A World Bank study found that businesses receiving digital payments are more likely to access credit because transaction records help banks assess their financial activity

-

The impact is strongest for small firms and businesses in low-income countries, where limited banking data often makes access to financing difficult

-

Africa’s rapid growth in mobile money and interoperable payment systems could help expand credit access and support small business financing

Digital payments are becoming increasingly central to business activity, particularly for small firms. A World Bank study published in January 2026 shows they go beyond saving time — they are also associated with better access to credit.

The report, titled "Firm Credit Constraints and Electronic Payments: A Global Analysis," notes that banks will not lend to businesses whose revenues, payment habits and commercial standing remain unknown to them. In Africa, where most business-to-business transactions are still conducted in cash, many merchants and traders remain largely invisible to banks. Without sales data or a verifiable track record, they struggle to obtain credit even when their business is thriving.

The study surveyed 48,581 firms across 101 countries and quantifies the scale of the problem. Across all countries studied, 14.78% of firms have no access to external financing, while another 16.23% have only partial access. In total, more than 30% of formally registered private-sector firms worldwide are cut off from the credit they need to grow.

The unexpected role of digital payments

The report finds that firms receiving payments digitally — via bank transfer, mobile money, card or similar methods — are significantly more likely to obtain credit than those operating exclusively in cash.

The mechanism is straightforward. When a customer pays by mobile money or bank transfer, the transaction leaves a digital record: date, amount and frequency. Accumulated over months or years, these data points give banks a clearer picture of a firm's revenue streams. To some extent, they can compensate for the lack of formal accounting records that many small African businesses do not maintain.

Receiving digital payments reduces by an average of 3.3 percentage points the probability that a firm is completely excluded from credit. That is equivalent to 22% of the average exclusion rate observed in the study.

The World Bank also specifies that receiving digital payments matters more than making them. Payment inflows directly reflect a firm's sales activity and the revenue it generates. That is the information banks rely on when deciding whether to extend credit.

Smaller firms benefit the most

The effect is strongest among the smallest firms, which are often the least visible to banks. For businesses with fewer than 20 employees, the reduction in the probability of being excluded from credit reaches 4 percentage points, compared with less than 2 points for larger firms. Companies with no formal accounting systems, no declared innovation activity or low productivity also benefit more from adopting digital payments.

At the country level, the effect is even more pronounced in low-income economies and those with underdeveloped credit registries. According to the report, the impact of digital payments on access to credit is nearly three times greater in poorer countries than in wealthy ones.

Where conventional tools for assessing borrowers are lacking, a digital transaction history can serve as a credible alternative.

Africa at the heart of the transformation

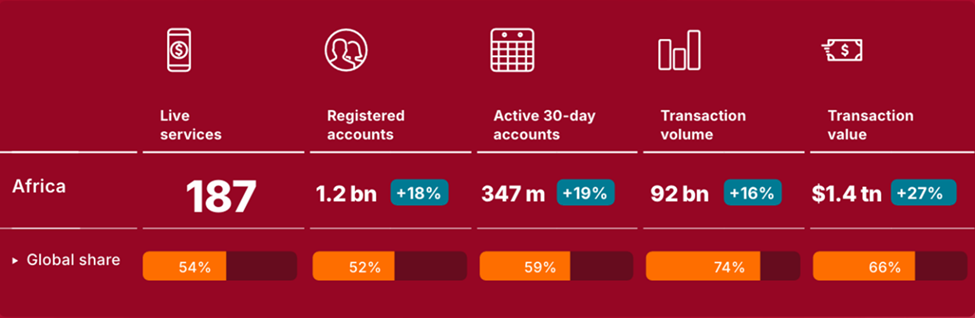

Africa combines two dynamics rarely found together: limited access to formal banking services and widespread adoption of mobile payments. According to the annual report of the Global System for Mobile Communications Association (GSMA), published in March 2026, more than $1.4 trillion passed through mobile money accounts in Africa in 2025, up more than 27% year-on-year. The continent accounts for 52% of all mobile money accounts worldwide and 66% of the global value of such transactions.

These flows represent a massive reservoir of information on firms' financial health that banks have only begun to exploit. Some fintech companies are already moving in that direction. In East Africa, 4G Capital uses mobile usage data to extend loans to small entrepreneurs. In Nigeria, platforms such as Moniepoint combine digital payment collection with lending services for small and medium-sized enterprises based on their payment histories.

Interoperability remains essential

For banks to make effective use of payment data, the information must be consolidated and accessible. A merchant receiving payments through several operators generates fragmented datasets that are difficult to aggregate. Interoperability — the ability of different payment systems to communicate with one another — therefore remains a key technical requirement.

Significant progress is under way. According to the "State of Inclusive Instant Payment Systems in Africa 2025" report by the AfricaNenda Foundation, published jointly with the World Bank, 36 instant payment systems were active across Africa in 2024, processing 64 billion transactions worth a combined $2 trillion. The report highlights growing interoperability across the continent. “Half of Africa's instant payment systems (IPS) now connect banks, mobile payment operators and fintechs through cross-domain platforms,” AfricaNenda states.

In the countries of the West African Economic and Monetary Union (WAEMU), the regional central bank has set Tuesday, June 30, 2026, as the deadline for all financial institutions to join the Interoperable Instant Payment System Platform (PI-SPI), a shared instant payment infrastructure launched in September 2025. This could mark an important step toward smoother transactions and broader access to credit.

The study provides African governments with a concrete policy argument: encouraging businesses to adopt digital payments is not only a modernization strategy, but also a tool for improving private-sector financing.

Three priorities emerge from the findings: accelerating the rollout of interoperable payment systems; encouraging banks to incorporate transactional data into credit assessments; and establishing clear rules governing the use of payment data so that businesses can share it with confidence.

Melchior Koba

- Mozambican financial services provider Letshego has launched a debit card in partnership with Mastercard.

- The card enables secure local and international transactions through Mastercard’s global payment network.

- The initiative aims to support digital transformation and financial inclusion in Mozambique’s cash-dominated economy.

Mozambican financial services provider Letshego has launched a debit card in partnership with Mastercard in Mozambique. The companies said the initiative aims to support the country’s digital transformation and strengthen financial inclusion.

In a statement published on Monday, May 11, Mastercard said the debit card operates on its global payments network. The card allows customers to conduct secure transactions both domestically and internationally wherever Mastercard services are accepted.

Moreover, the card supports everyday payments and enables broader participation in the formal financial system. The initiative comes amid accelerating digital transformation and growing demand for digital payment solutions in Mozambique.

Consumers increasingly use international e-commerce platforms such as Alibaba and Jumia, while others subscribe to streaming services including Netflix and Spotify. However, many unbanked consumers still face difficulties accessing online payment services and digital financial tools.

“By giving more people the tools they need to participate in the digital economy, we help strengthen financial resilience and enable communities to thrive in an increasingly connected world,” said Gabriel Swanepoel, division president for Africa at Mastercard. The initiative also targets small and medium-sized enterprises, which remain a central pillar of Mozambique’s economy.

Reliable digital payment tools can help SMEs expand online sales, secure transactions with customers and suppliers, and access new markets, including international markets. Furthermore, digital payment systems can help formalize economic activity and improve the traceability of financial flows in an economy where cash still dominates a large share of transactions. However, service availability alone may not guarantee widespread adoption of digital financial services.

Several factors continue to influence adoption rates, including user trust, digital literacy levels, access to smartphones and internet connectivity, and service costs. In addition, entrenched consumer payment habits and the persistent use of cash across many segments of the economy could slow adoption.

This article was initially published in French by Isaac K. Kassouwi

Adapted in English by Ange J.A de Berry Quenum

Despite its leading role in advancing financial inclusion on a continent where banking penetration remains low, mobile money still faces major structural barriers that limit its full potential. Yet the service, which continues to expand with new offerings, particularly in banking, has the capacity to transform household economies and the broader financial landscape in Africa.

Africa's mobile money sector recorded strong growth in 2025, yet barriers to full adoption persist for millions across the continent.

Nearly $1.432 trillion flowed through mobile money accounts in Africa in 2025, up roughly 27% from 2024, according to the "State of the Industry Report on Mobile Money 2026," published Tuesday, March 24, by the GSMA, the global association of mobile network operators.

The continent accounted for nearly 66% of the $2.091 trillion in global mobile money transaction value, which itself rose 23% year on year. Africa also represented around 74% of the 125 billion mobile money transactions recorded worldwide, roughly 92 billion operations, up 16% from 2024.

The report also noted that Africa is home to 52% of mobile money accounts globally. At end-2025, the continent had approximately 1.2 billion accounts, up 18% from 2024, with 347 million active on a monthly basis. Worldwide, total accounts reached around 2.3 billion, up 13%, with 593 million active over a 30-day period.

Africa remains the epicenter of mobile finance. But this success masks a growing contradiction: the service is expanding rapidly while full adoption across the population and its real impact remain limited.

Barriers to inclusion

The first barrier is access to devices. The World Bank notes that 84% of adults in developing countries own a phone, but roughly one quarter of them still use a basic handset, "more affordable, with limited features and no internet browser." Only two-thirds of adults therefore own a full smartphone enabling access to apps and browsers. In sub-Saharan Africa, that figure drops to 33%. In that region, as in South Asia, the most commonly cited reason for not owning a smartphone is cost. The International Telecommunication Union (ITU) has also highlighted that across the African continent, one of the main obstacles to the adoption of digital services remains affordability, particularly that of devices.

The second barrier is digital financial literacy. The GSMA's 2026 mobile money report is explicit: low digital financial literacy remains a major obstacle to the adoption and use of the service. In African countries surveyed where uptake gaps persist, the data are clear. In Ethiopia, among people who are aware of mobile money but do not have an account, 60% of women and 54% of men say they do not know how to use the service; 45% of women and 50% of men say they struggle to use a phone or fear making mistakes. In Egypt, this barrier affects 21% of women and 15% of men; in Nigeria, 22% of both women and men. Compounding this, in Ethiopia, 24% of women surveyed cite the lack of a SIM card or phone as an obstacle.

Beyond the service, a human impact

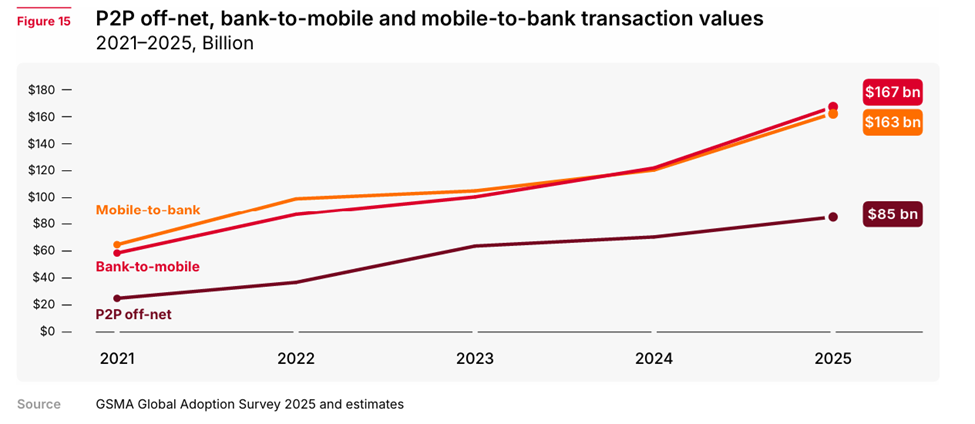

A clear paradox emerges: mobile money first took hold through the most basic handsets. But its new frontier now demands more than a simple mobile phone. The range of use cases has expanded, and service providers increasingly rely on super-apps rather than USSD codes to deliver greater value, including bill payments, government social transfers, micro-insurance, micro-credit and micro-savings. The most dynamic segments are now merchant payments, up 42% to $155 billion in 2025, and interoperable transfers between banks and mobile wallets, at $167 billion. In other words, the sector has moved well beyond the simple peer-to-peer transfers of its early days, advancing into a more sophisticated phase where users must navigate interfaces, options, QR codes, virtual cards, security features and transaction records. Without adequate devices or basic digital fluency, a portion of Africans risk being confined to the most elementary uses as the ecosystem moves toward more complex services.

This divide is also social and gendered. Without suitable phones and basic digital skills, millions of Africans remain on the margins of what mobile money can offer. In low- and middle-income countries, the GSMA estimates that women remain 14% less likely than men to use mobile internet, leaving 885 million women still unconnected, of whom approximately 60% live in South Asia and sub-Saharan Africa. This creates the risk of a two-speed financial inclusion, uneven in practice.

Unlocking the full potential of mobile money in Africa therefore requires more than a commercial response. It must be industrial, educational and regulatory. The ITU advocates for cheaper entry-level smartphones, purchase options facilitated through microcredit or installment payments, lower costs for handsets and data, and the integration of basic digital skills into school curricula and training programs. The GSMA report echoes this view, stressing the need for digital financial literacy initiatives targeting women, rural populations and older people. The World Bank notes that cost, ease of use and security must be addressed together. The real challenge for Africa is no longer to prove that mobile money works, it is to ensure that everyone can genuinely use it.

Muriel Edjo

-

GSMA will award grants of £100,000 to £200,000 ($135,000 to $270,000) over 15 to 18 months.

-

The fund targets Africa, Central and South America, and South and Southeast Asia.

-

Eligible startups must provide at least 25% co-financing of total project costs.

The Global Association of Mobile Network Operators (GSMA) announced on Sunday, February 23, the launch of an Innovation Fund to support small enterprises and startups that use mobile technologies to advance clean energy transition and digital inclusion. The initiative targets Africa, Central and South America, as well as South and Southeast Asia.

GSMA will provide grants ranging from £100,000 to £200,000 ($135,000 to $270,000) over a period of 15 to 18 months. The organization designed the fund to back commercially viable solutions that combine environmental impact with business sustainability.

“We invest in companies that use mobile technology to strengthen digital inclusion and support a sustainable energy transition, while offering circular solutions that extend device lifecycles and make connectivity more affordable for underserved communities,” said Philippe Bellordre, Acting Head of Mobile for Development at GSMA.

Eligible companies must register legally in one of the targeted regions, employ up to 250 people and demonstrate both revenue generation and an active user base. The fund requires beneficiaries to contribute at least 25% of total project costs through matching financing.

The program will support initiatives such as device repair, refurbishment and reuse, as well as trade-in programs and responsible collection and recycling of electronic waste. These solutions aim to extend device lifespans, reduce e-waste and improve connectivity affordability for underserved populations, thereby strengthening socio-economic inclusion.

In addition to financial support, selected startups will receive ongoing monitoring, evaluation and learning assistance, as well as increased visibility through GSMA publications and platforms.

Applications will remain open until April 6, 2026 at 23:59 UK time. Interested companies can submit applications through the dedicated online portal.

https://gsma-innovation.fluxx.io/user_sessions/new

This article was initially published in French by Samira Njoya

Adapted in English by Ange J.A de Berry Quenum

- Algeria introduces electronic stamp duty payments for commercial register filings

- “Tabaakoum” platform enables card-based payments and digital receipt acceptance

- Move supports digitalisation, transparency, and reduced informal economic activity

Algeria’s finance ministry and trade ministry have signed a protocol to introduce electronic stamp duty payments for commercial register filings, the two ministries said in a joint statement on Wednesday.

The agreement enables the use of the “Tabaakoum” digital payment platform for stamp duties linked to commercial registration. Payments can be made via interbank cards or the state-backed Edahabia card.

The digital receipt generated by the platform will now be accepted as official documentation for business registration or modification filings. The move aims to offer more flexibility to businesses and increase the transparency of financial transactions.

The initiative comes as electronic payments see rapid growth in the country. Data from the Monetics Group (GIE Monétique) shows more than 5.2 million payments via electronic terminals between January and July 2025 generated nearly 47.2 billion dinars ($363.8 million), a total that already exceeds all of 2024.

Beyond simplifying procedures for merchants and entrepreneurs, the shift to electronic payments for the commercial register is part of a broader national strategy to modernize public services and reduce the informal economy. The government has recently launched multiple initiatives to expand digital payments, encourage e-commerce and improve online service access in a country where internet penetration now reaches about 77% of the population.

By facilitating commercial registration and reducing the costs and delays linked to in-person procedures, the state aims to improve the competitiveness of the entrepreneurial sector and enhance the traceability and transparency of economic activity.

Samira Njoya

-

Trésor Pay digitizes the payment of fees and charges owed to the state

-

The platform aims to improve revenue collection and reduce fraud risks

-

Payments can be made via mobile money alongside existing channels

Guinea has launched Trésor Pay, a digital platform designed to dematerialize the payment of administrative fees and charges owed to the state. The platform was officially rolled out on December 22 in Conakry and is intended to improve public revenue mobilization while reducing administrative friction for users.

According to Economy and Finance Minister Mourana Soumah, Trésor Pay follows a presidential directive aimed at improving citizens’ access to public services and strengthening domestic revenue collection. The platform is expected to reduce queues, limit costly travel, and curb informal practices, while ensuring better traceability of payments. For the state, the dual objective is to speed up the availability of funds and reduce fraud risks across the collection chain.

Operationally, Trésor Pay allows users to pay administrative fees and charges collected by the public treasury directly via their mobile phones. The platform relies on electronic money services and operates alongside the traditional payment circuit. It also includes user support mechanisms, notably a dedicated call center, to assist citizens with the payment process and ensure service continuity.

The rollout comes at a time when financial inclusion in Guinea remains limited, with an estimated rate of around 30%, while the use of mobile money continues to expand rapidly. In this context, the digitalization of public payments is seen as a tool to widen access to administrative services, particularly for populations living far from urban centers and outside the traditional banking system. The reform forms part of broader efforts by the authorities to modernize public finances and strengthen economic governance.

Over time, Trésor Pay could help improve the collection of non-tax revenues, shorten payment processing times, and reduce fraud risks. The platform also opens the door to additional uses, including mass payments and other dematerialized public financial instruments. For Guinea, the challenge now is to turn Trésor Pay into a fully operational system capable of sustainably supporting budget efficiency and transparency in public action.

Samira Njoya

- Ethiopia launches 2026-2030 digital payment strategy and instant system Ethiopay

- Strategy targets inclusion, security, and cross-border retail payment access

- Digital reforms support AfCFTA integration and process $119 billion annually

Ethiopia has launched a national digital payment strategy and a new instant payment system as part of efforts to modernize its financial system and expand access to digital services, particularly among underserved populations.

The National Digital Payment Strategy (NDPS) for 2026-2030 is a five-year roadmap aimed at strengthening interoperability, trust and innovation in payments. It includes plans to facilitate low-value retail cross-border transfers through cards, mobile wallets and digital banking services. The strategy also prioritizes system security, interoperability between providers and consumer protection, while seeking to narrow usage gaps between urban and rural areas and between men and women.

The instant payment system, known as Ethiopay, was developed by national operator EthSwitch. It provides a secure and interoperable infrastructure for instant peer-to-peer transfers, QR code payments, bulk payments and selected cross-border transactions, making it the backbone of Ethiopia’s domestic digital payments system.

The initiatives build on Ethiopia’s broader Digital Ethiopia 2025 and Digital Ethiopia 2030 programmes, which aim to transform economic, administrative and social systems through digital technology. These programmes focus on modernizing public services, improving connectivity and expanding the role of private-sector operators.

Officials say the reforms are already delivering results, with more than 18.5 trillion birr ($119 billion) processed annually through digital platforms. The entry of Safaricom Ethiopia with M-Pesa, the rollout of Ethio Telecom’s Telebirr and the gradual integration of the national digital identification system, Fayda, have contributed to the development of the digital payments ecosystem.

The rollout of the NDPS and Ethiopay is expected to simplify everyday payments, support financial inclusion and streamline commercial transactions. It is also expected to play a strategic role in regional integration by allowing Ethiopia to more quickly benefit from the African Continental Free Trade Area (AfCFTA).

The AfCFTA covers 1.4 billion people and has a combined gross domestic product of $3.4 trillion, according to its Secretary General, Wamkele Mene.

Samira Njoya

Strategically located between Europe and Africa, Morocco has leveraged its geographical position and its well-educated youth to develop its services economy. The digital sector is now a major beneficiary of this approach, offering considerable opportunities for international businesses.

Exports of digital and outsourced services have emerged as a quiet engine of Morocco’s economy, reaching 26.2 billion dirhams ($2.8 billion) in 2024. According to Morocco’s foreign exchange office, Office des Changes, this is a slight 0.2% increase from 2023. The sector’s growth momentum was confirmed in the first half of 2025, with exports hitting 13.4 billion dirhams, a 3.5% rise compared with 12.9 billion dirhams during the same period in 2024.

The sector’s growth momentum was confirmed in the first half of 2025, with exports hitting 13.4 billion dirhams

Digital service exports involve specialized Moroccan teams providing services to foreign companies and clients. These local teams execute advanced digital tasks, or international companies outsource support and customer service activities to Moroccan providers to reduce operating costs. Digital services are the most dynamic and in-demand component, generating the majority of the sector's export revenue.

The sector is predominantly driven by Information Technology Outsourcing (ITO) and Customer Relationship Management (CRM). In 2024, IT and technology services, which encompass development, maintenance, and cybersecurity, accounted for 40.3% of the total. CRM and call center activities, which handle assistance and multilingual support, followed closely at 37.4%. Together, these two segments represent 78% of total digital service exports.

Other key segments contribute to the growth: Engineering Services Outsourcing (ESO), which includes design and systems integration, accounted for 13.2% of revenue. Business Process Outsourcing (BPO), covering back-office functions like accounting and data entry, made up 8.9%. Meanwhile, Knowledge Process Outsourcing (KPO), which focuses on high-value tasks such as financial analysis and business intelligence, was the smallest component at 0.2%.

Despite global tensions, including inflation and exchange rate volatility, Engineering Services Outsourcing (ESO) revenues grew, a sign of Morocco’s gradual move up the value chain. ESO receipts rose from 3.2 billion dirhams in 2023 to 3.4 billion in 2024, already reaching 2.5 billion dirhams in the first half of 2025.

Despite global tensions, including inflation and exchange rate volatility, Engineering Services Outsourcing (ESO) revenues grew, a sign of Morocco’s gradual move up the value chain

Business Process Outsourcing (BPO) also grew, rising from 1.9 billion dirhams to 2.3 billion dirhams between 2023 and 2024, with 1.3 billion dirhams generated in the first half of 2025. Conversely, Knowledge Process Outsourcing (KPO) experienced a sharp decline, falling from 78 million to 48 million dirhams, and totaled 21 million dirhams in the first half of 2025.

The sector’s stability in 2024 and positive signals in 2025 support Morocco's foreign exchange earnings and its export diversification beyond goods. The acceleration of engineering services demonstrates that Morocco is asserting itself as an engineering hub near Europe, offering reduced lead times and compliance with international standards, rather than solely a call center platform.

The growth in outsourced digital services translates into stable revenue and qualified jobs for the Moroccan economy. Call centers and support activities recruit young people with strong language and interpersonal skills. IT and technology services, however, stimulate demand for more technical and better-paid profiles. The Ministry of Digital Transition and Administrative Reform reported the sector already supported 141,000 jobs in 2023, up from 130,000 in 2022 and 100,000 in 2020.

The acceleration of engineering services demonstrates that Morocco is asserting itself as an engineering hub near Europe, offering reduced lead times and compliance with international standards, rather than solely a call center platform

To better manage this growth trajectory, the Office des Changes and the Ministry of Digital Transition have launched a project to modernize monitoring indicators for digital service exports. The goal is to obtain more granular data to target training, regional attractiveness, and promising niche markets. This work is part of the Digital Morocco 2030 strategy.

To maintain this growth, Morocco must tackle three key challenges: adapting to the era of automation by ensuring continuous upskilling to maintain competitiveness against artificial intelligence; guaranteeing high quality service, robust cybersecurity, and impeccable business continuity to compete internationally; and finally, developing talent and infrastructure across the country. Attracting higher value-added projects requires a broader pool of skilled talent and a regional network of infrastructure extending beyond major cities. Coordinated execution of these reforms across government actors will be key to success.

Muriel Edjo

• Mobile money and online banking are driving digital finance growth across Africa.

• Interoperable systems in Ghana, Nigeria, and Kenya show strong adoption and economic impact.

• Challenges remain with digital access, cybersecurity, and regulatory harmonization.

Africa’s financial sector is undergoing rapid change with the rise of mobile money and digital banking. At the center of this shift, interoperable instant payments -systems that enable transactions across banks and mobile operators- are emerging as a key driver of financial inclusion and regional trade.

According to the World Bank, about 350 million adults in sub-Saharan Africa remain unbanked. Mobile money has helped bridge part of this gap, with 44% of adults holding an account in 2024, compared with the global average of 29%, the latest Global Findex 2025 report shows.

Several countries have taken major steps to build interoperable payment systems. In Ghana, the GhIPSS platform connects banks and mobile operators, handling an average of 17.9 million instant transactions per month since December 2022, involving more than 55 financial institutions.

In Nigeria, the NIBSS platform processed interbank instant payments worth 600,360 billion nairas (around $390 billion) in 2023. In Kenya, M-Pesa continues to dominate, accounting for nearly 55% of GDP, according to the Fintech Association of Kenya.

More recently, Sierra Leone, the Comoros, Somalia, and Algeria have announced national interoperable payment systems, adding to the continent’s growing financial infrastructure.

These efforts also support the African Continental Free Trade Area (AfCFTA) by making cross-border transactions cheaper and faster. The Pan-African Payment and Settlement System (PAPSS) reflects this trend, enabling central banks and financial institutions to make real-time payments in local currencies, lowering costs and delays while deepening integration. According to the GSMA, mobile money transactions in sub-Saharan Africa reached $190 billion in 2023, or 4.5% of regional GDP, up from $150 billion in 2022.

Challenges ahead

Interoperable instant payment systems are boosting financial inclusion, lowering transfer costs, encouraging fintech and e-commerce innovation, and strengthening regional integration. They also help states track financial flows and secure transactions, reinforcing digital sovereignty.

But hurdles remain. The digital divide is still wide, especially in rural areas with weak Internet coverage. Cybersecurity risks such as fraud, hacking, and data theft continue to undermine trust. And the lack of harmonized regulations slows the rollout of cross-border solutions.

To unlock the full potential, African countries need to expand digital infrastructure, step up cybersecurity, train populations in digital finance, and move toward unified regulation. With smartphone penetration in sub-Saharan Africa projected to reach 87% by 2030, these initiatives could bring millions into the financial system, support intra-African trade, and speed the transition toward an integrated digital economy.

While millions of Africans have embraced mobile money for savings, its adoption for credit remains modest. This is primarily due to the persistence of informal lending practices, even as new innovations begin to emerge.

Mobile money has become a transformative force for financial inclusion in Africa, yet its full potential remains untapped. While the service has excelled at providing a platform for savings, it has made little headway in providing widespread access to credit. The Global Findex Database 2025, published by the World Bank, shows the share of African adults with a mobile money account soared from 27% to 40% in just three years, reaching the highest rate globally. The report found that 23% of African adults saved using their mobile accounts in 2024, nearly double the rate of 13% in 2021.

The report also shows that 35% of African adults overall reported saving digitally or through traditional institutions. In countries with large mobile money economies like Ghana, Kenya, Senegal, and Uganda, more than 50% of adults use mobile money for savings, signaling a massive adoption of the service.

Mobile money is more accessible than traditional banking networks, making it easier to save small amounts and providing flexible deposits and withdrawals through local agents. This has led to more inclusive adoption, especially in rural and informal settings.

Savings Succeed, Credit Stalls

Despite the success of savings, access to credit through mobile money remains very limited. In 2024, only 7% of African adults borrowed through their mobile accounts, a figure that has remained stable since 2021. By contrast, nearly 59% of adults across the continent used some form of credit, though primarily through informal means like family or savings clubs.

In major mobile money markets like Kenya, Ghana, and Uganda, 22% to 32% of adults have borrowed through a mobile operator. However, these loans are typically small, short-term, and often carry high interest rates, which limits their overall economic impact.

Several factors explain this disconnect. According to the World Bank, regulatory authorities remain cautious, fearing over-indebtedness or fraud. The organization also points to business models that favor less-risky deposits and payments over credit.

The report also reveals that customers themselves are hesitant to borrow through platforms not well known for lending due to distrust, limited financial literacy, or overly strict eligibility simulators.

Innovations and Lingering Limits

While some specialized fintech and mobile platforms are gradually expanding their offerings through alternative credit scoring and nano-loans for micro-entrepreneurs, a mass-market for inclusive digital credit has yet to emerge. The report notes that countries with close cooperation among mobile operators, banks, and regulators, such as Kenya, are making progress, but elsewhere, advancement is slow.

The challenge now is to pair access to digital savings with policies for financial literacy, consumer protection, and regulatory innovation. The goal is to advance credit access without making already vulnerable populations more fragile.

For the World Bank, mobile money's full potential in Africa will only be unlocked when it contributes as much to productive investment as it does to savings security. This requires building customer trust and analytical skills regarding digital credit offers, improving interoperability between services and institutions, and adapting credit to local economic realities while minimizing associated risks.

Melchior Koba

More...

• Burundi deepens collaboration with Liberia, Sierra Leone, and Benin on tax digitalization

• OBR targets simplified tax processes, better data management, and online platforms

• National rollout of electronic billing and integrated tax systems underway

Burundi’s tax authority (OBR) is accelerating its digital modernization efforts by learning from other African countries. Late last week, the OBR hosted two days of discussions with Sierra Leone’s National Revenue Authority (NRA), known for successfully implementing a digital tax collection system.

This initiative follows a similar exchange organized about a week earlier with Liberia’s Revenue Authority (LRA). Over two days, LRA experts shared their experience with Burundi’s e-KORI project, which focuses on the digitalization of internal tax collection. OBR praised Liberia’s success in building an effective digital tax system following years of civil conflict. The OBR also confirmed ongoing cooperation with Benin on similar reforms.

Burundi’s digital tax strategy aims to simplify processes for taxpayers, automate revenue management and collection, and improve data reliability. One of the most notable milestones so far has been the launch of an online filing and payment platform in 2023. The OBR website also provides services such as anonymous reporting of corruption, document verification, and access to regulatory information.

The government is now working on implementing an integrated digital system for managing internal taxes and non-tax revenues. A tender for this project was launched on May 5. At the same time, the OBR is stepping up efforts to promote the use of electronic billing machines among taxpayers.

The OBR’s digital transformation plan aligns with international standards. The Organisation for Economic Co-operation and Development (OECD) emphasizes that digitalizing tax administrations reduces the cost and complexity of paying taxes. “When the process is tedious, it creates significant time and financial costs for taxpayers. At the macro level, this can lead to major productivity and resource losses,” says the OECD.

However, the OBR recognizes that technology alone is not enough. The authority highlights the need for a clear and consistent tax framework, stronger public awareness of tax compliance, and improved monitoring of how taxpayers use digital tools such as billing machines and online platforms.

Beyond digital systems, access to technology remains a critical challenge. For example, according to the International Telecommunication Union (ITU), nearly 90% of Namibians did not use the Internet in 2023, and around 80% of the population lacked mobile phones.

The OBR believes improving access to digital infrastructure will be key to ensuring that taxpayers across Burundi can fully benefit from its digital tax services.

• Madagascar launches e-Ariary pilot to modernize payments

• Designed for mobile phones and offline use, the currency supports everyday transactions

• The trial involves banks, public services, vendors, and more.

Madagascar's central bank launched a 10-month pilot program for its digital currency, the e-Ariary, on Friday, May 23, aiming to modernize the financial system and boost inclusion across the island nation. The initiative seeks to reduce reliance on physical cash, lower transaction costs, improve financial traceability, and expand access to financial services, particularly in rural areas.

"We hope that, by the end of this process, the use of banknotes will decline, as managing them is very expensive for the Central Bank," said Aivo Andrianarivelo, Governor of the Central Bank of Madagascar. He noted that the 100 Ariary note, equivalent to about $0.022, does not even cover its printing cost and has a short lifespan of approximately six months, requiring frequent replacement that Madagascar cannot undertake domestically.

The e-Ariary is designed for broad accessibility, usable via smartphones, basic mobile phones, and offline methods such as QR codes, smart cards, and point-of-sale terminals. Its primary applications will include everyday transactions like merchant payments, transportation fares, salary disbursements, and social transfers, with an emphasis on affordability for all users.

The digital currency is intended to complement, rather than replace, existing financial tools, particularly mobile money platforms, which will continue operating in parallel. In 2023, Madagascar recorded over 10 million mobile money accounts, significantly outnumbering the 3 million traditional bank accounts. Mobile money platforms facilitated nearly 342 million transactions totaling 38,161 billion Ariary (approximately $8.5 billion USD), underscoring the increasing prominence of digital services in the country's financial landscape.

The pilot program will rigorously test the technical infrastructure, transaction security, and priority use cases of the e-Ariary. It will also assess the digital currency’s broader socio-economic impact. A diverse group of stakeholders is participating in the trial, including commercial banks, microfinance institutions, state-run entities such as the utility company Jirama, market vendors, the Treasury, and the tax administration.

Central to the rollout will be extensive user awareness campaigns, as public understanding and confidence are considered vital for the successful adoption of the e-Ariary. If successful, the project is expected to usher in a new era of digital payments in Madagascar, establishing a more inclusive, transparent, and interoperable financial ecosystem while supporting ongoing efforts to formalize the economy.

By Samira Njoya,

Editing by Sèna D. B. de Sodji

• Ethiopia launches Fayda Wallet to boost digital inclusion

• Developed by NIDP in partnership with TECH5 and Visa, the wallet uses advanced biometric and identity technologies to enable secure online/offline verification

Ethiopia officially launches Fayda Wallet, a digital wallet backed by the national biometric ID, designed to simplify access to financial and administrative services.

Presented during the ID4Africa 2025 conference, which concluded on Friday, May 23 in Addis Ababa, the wallet was developed by the National ID Program (NIDP) in partnership with TECH5 and Visa.

“We are thrilled to support the launch of the Fayda Wallet, a groundbreaking initiative that will significantly enhance financial inclusion and streamline digital transactions in Ethiopia. This collaboration underscores Visa’s commitment to empowering communities through innovative digital payment solutions,” said Yared Endale, Visa’s General Manager for East Africa.

The launch of Fayda Wallet is part of Ethiopia’s Digital Strategy 2025, which aims to assign a digital identity to 70 million people by 2028. Through this application, users can generate a secure digital identity certificate (VC) from the Fayda ID system. This certificate, aligned with Self-Sovereign Identity (SSI) principles, enables secure verification, both online and offline, to access a variety of services including payments, public services, and, account opening.

The wallet is based on advanced technologies, including TECH5’s T5-AirSnap and T5-OmniMatch for contactless biometric capture and matching, as well as KeyShare Wallet for secure digital identity management. It also allows users to access instant banking services, such as account opening via biometric eKYC and the issuance of a virtual Visa card. The Cooperative Bank of Oromia (Coopbank) is the first to have integrated this solution.

To ensure broader digital inclusion, Fayda Wallet also offers agent-based access points, allowing citizens without smartphones to access digital services using their biometric data, in compliance with W3C standards and the European Union’s eIDAS frameworks.

In a country where less than 47% of adults had a bank account in 2022, according to the World Bank, the launch of Fayda Wallet could transform access to essential services and strengthen trust in digital interactions.

By Samira Njoya,

Editing by Sèna D. B. de Sodji

The collaboration underscores a shared commitment to tackling unemployment, reducing poverty, and building a digital-ready workforce equipped for the demands of the modern global economy.

The Federal Government is partnering with the World Bank to drive a shared agenda focused on creating high-quality jobs for young Nigerians. The Minister of Finance and Coordinating Minister of the Economy, Mr. Wale Edun, confirmed this during the World Bank/IMF Spring Meetings, according to a statement issued by the Ministry of Information on April 25.

Speaking to journalists in Washington, D.C., Mr. Edun highlighted that Finance Ministers from World Bank member countries had collectively agreed to prioritize employment generation as a key pillar of development. "Creating good-quality jobs is central to addressing poverty and inequality," the Minister said.

A major element of this strategy includes the expansion of Nigeria’s digital infrastructure, ensuring broader access to internet services, data, and fibre-optic networks, to empower young Nigerians to participate actively in the digital economy.

According to the World Bank, Nigeria’s poverty rate climbed to 38.9% in 2023, with approximately 87 million Nigerians living below the poverty line. The bank pointed to sluggish economic growth as one of the key drivers of this worsening poverty situation. However, it also noted that targeted economic reforms could help reverse the trend. The Federal Government’s new partnership with the World Bank - particularly its focus on creating youth jobs using digital tools - directly addresses the urgent need for inclusive economic recovery.

By investing in digital infrastructure and skills development, Nigeria can equip its large youth population with tools to access new economic opportunities, especially in the growing global digital economy. This approach not only has the potential to reduce youth unemployment but also to lift millions out of poverty by stimulating entrepreneurship, remote work, and tech-driven sectors.

Hikmatu Bilali